The Conversation That Doesn't Happen

A proven way to finance risk has been around for forty years. Most companies that qualify still never get it explained clearly enough to weigh it. This is where I try to fix that — one week at a time.

Welcome to The Risk Finance Alternative. These are my (Zeb Holt) own views, written in my own name — not those of any employer or client.

Picture a company you’d call well run. Fifteen years in business, a clean loss history, a safety culture that actually means something on the floor. Every year, a few weeks before renewal, it gathers its loss runs, takes a quote, negotiates at the margins, and signs. The number goes up a little or down a little. The process repeats.

Inside that company is risk that is stable, predictable, and well managed — exactly the kind of risk a business could choose to finance more efficiently itself. The option to do that exists. It is not exotic. It has been used by the largest companies in the world for more than forty years. And yet, in most companies like the one I just described, the conversation about whether to use it never happens.

Not because the answer would have been no. Because no one ever fully understood it was on the table.

That gap — between a proven option and a company that never seriously weighs it — is what I want to write about here, every week.

What “the alternative” actually is

When people hear “alternative risk finance,” they often reach for the vehicles: captives, group captives, cells, risk retention groups, fronted programs. Those matter, and we’ll get into all of them. But the vehicles aren’t the idea. The idea is simpler and more useful than the jargon makes it sound.

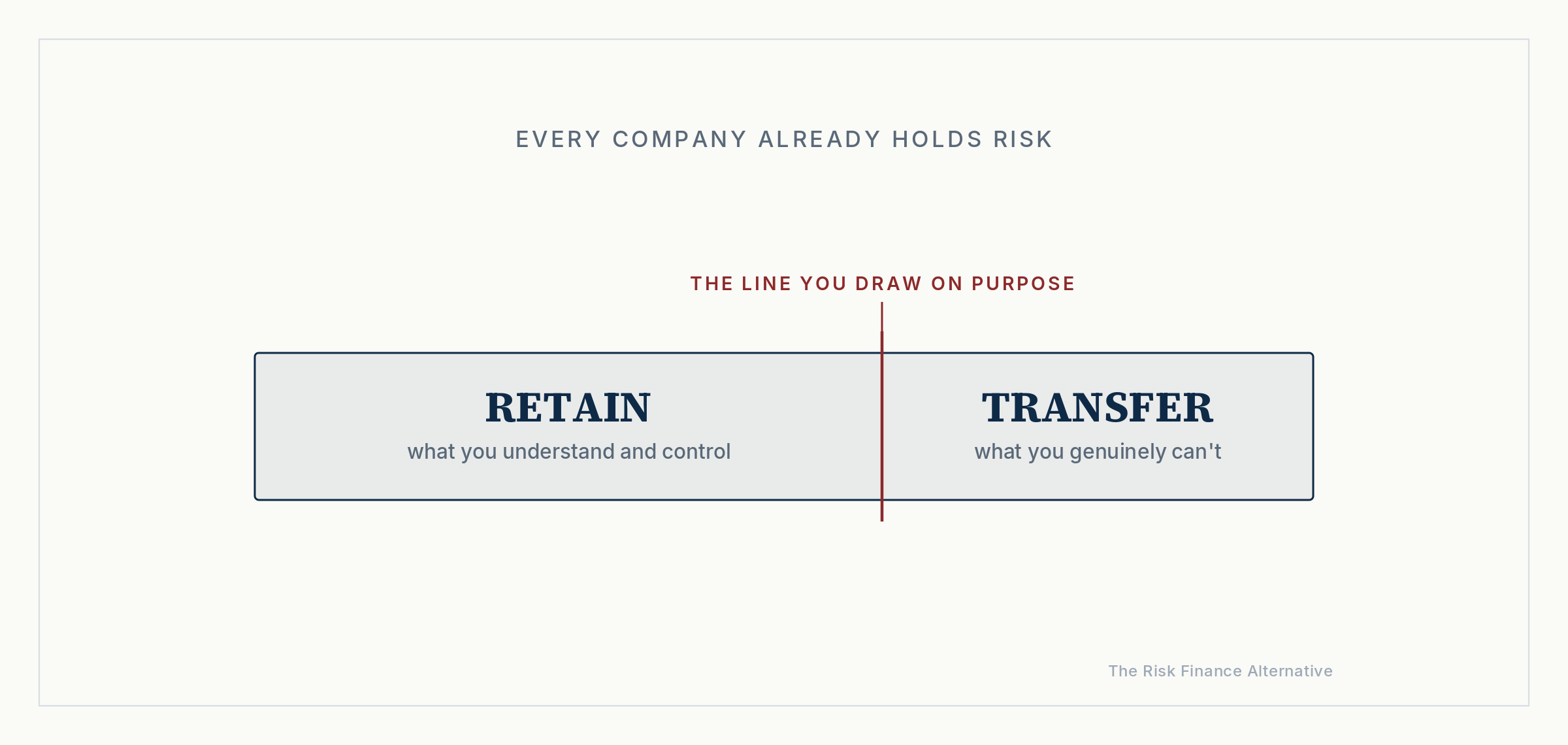

Alternative risk finance is a different way of deciding how to fund the risk you already carry. Every company holds risk whether it names it or not. The conventional approach is to transfer as much of it as possible to an insurer and treat the premium as a cost of doing business. The alternative approach asks a sharper question: which of these risks do we actually understand and control well enough to finance ourselves, and which should we genuinely transfer? Retain what you can manage. Transfer what you can’t. Be deliberate about the line between the two.

That’s it. Everything else — the structures, the domiciles, the actuarial work — is machinery in service of that one decision about choice and control.

The largest companies have been making that decision deliberately for decades. The question that interests me is why its understanding thins out so quickly the moment you move below the top of the market.

Why the option goes unexamined

After enough years around this, I’ve stopped believing the gap is about fit. Plenty of companies that never look at the alternative would qualify for it comfortably. The gap is somewhere else, and I think it comes down to three honest things.

The first is that this is genuinely complex. The alternative asks a company to think like a risk financier rather than a coverage buyer — to get comfortable with actuarial credibility, capital, collateral, governance, and a multi-year time horizon instead of an annual one. That’s a real learning curve. Complexity is a perfectly legitimate reason a good option goes unexamined. It isn’t anyone’s failing; it’s just hard.

The second is that the alternative is nobody’s default. The status-quo renewal is the path of least resistance for everyone involved, the buyer included. Looking seriously at a different structure takes deliberate effort and time that a busy CFO has to actively choose to spend, usually against a dozen things that feel more urgent. Inertia is quiet and powerful, and it wins most years.

The third is that the education is uneven. Where someone has had this explained to them clearly — patiently, in plain language, with the math made legible — they tend to engage with it, and a meaningful share go on to use it. Where they haven’t, the option simply stays invisible. The differentiator, over and over, is understanding. Not suitability.

The more of this market I see, the more convinced I am that the binding constraint isn’t whether companies qualify. Plenty do. The constraint is that the alternative is hard to understand and easy to never get around to. And that is a problem education can actually solve. That’s most of why I’m writing this.

Why now, and why me

I’ve spent more than twenty years in alternative risk and alternative capital — across group captives, cells, single-parent captives, risk retention groups, fronted programs, and reinsurance, onshore in the U.S. and offshore around the world. In that time I’ve watched the alternative work for companies that committed to understanding it. I’ve also watched far too many qualified companies never get a clear, honest explanation of what it even was.

I don’t think that’s anyone’s fault. I think it’s an information problem. And information problems are worth writing about.

To be clear about the boundaries: everything here is my own perspective, offered in my own name. None of it speaks for my employer or anyone’s clients, and none of it will trade on anything I can only see from where I happen to sit. The goal is to share what’s broadly true about this market, in language anyone can follow.

What this newsletter will be

My plan is one issue a week, focused on three things: building awareness that the alternative exists, explaining how it actually works without the jargon, and helping you assess — honestly — whether it’s worth a closer look for a given situation. Some weeks that means demystifying a single concept. Some weeks it means a question worth sitting with. Some weeks it means a concrete signal that a company should at least run the analysis.

I’d also like this to be a conversation rather than a broadcast. If you’re a CFO, a risk manager, a broker, a captive manager, or a regulator, you see things I don’t, and I’d rather be sharpened than agreed with. Reply to any issue. I read them.

The company I started with — the well-run one renewing on autopilot — isn’t doing anything wrong. It’s doing the normal thing. I just think there is almost always an alternative worth understanding, and most people never get it explained clearly enough to weigh it. That’s what this is about.

One question I’m sitting with

If the gap really is understanding rather than fit, then the most valuable thing isn’t a better product — it’s a clearer explanation. So here’s what I keep turning over: what’s the one thing about alternative risk finance that someone tried to explain to you, and it just never clicked? That’s probably where I should start. Tell me, and I’ll write it.

Zeb I appreciate your willingness to do this. I’m looking forward to your insights. As a broker, I am a big fan of alternative risk financing solutions. It’s something that i think the market as a whole is going to seriously consider as casualty rates continue to increase across a number of industries.